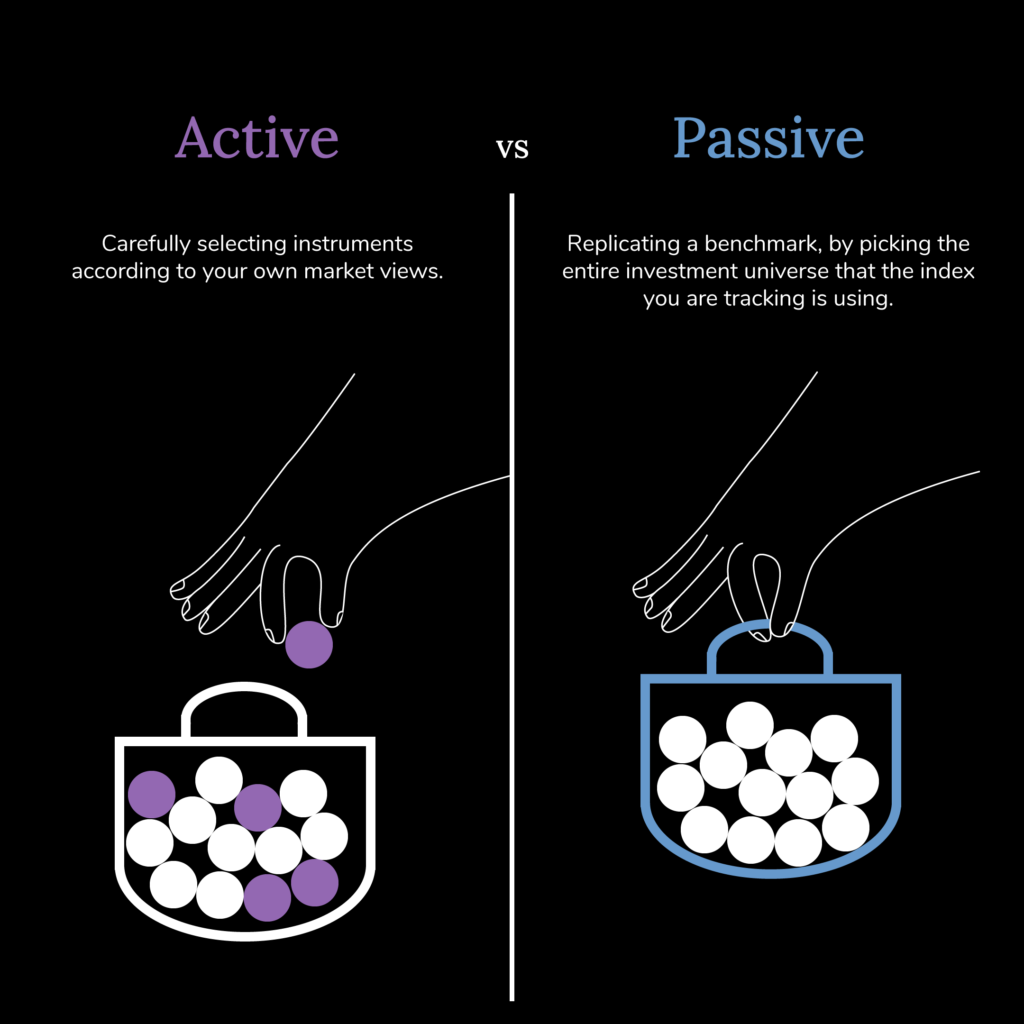

Have you ever wondered what the difference between passive and active investment products is?

We generally talk about passive investment products for funds, which are baskets of securities that are passively following a given benchmark. This means buying the underlying assets that a benchmark buys, and selling the ones that it sells.

On the contrary, active investment products often refer to funds that have a Portfolio Manager making active decisions on the constituents of the funds, with a goal to outperform the benchmark. This can be by following a specific investment strategy and/or applying their market views to the portfolio.

If a portfolio manager is successful and outperforms their benchmark, we say that they generated “alpha”. Another term for alpha is “excess return”, referring to the return generated above a given benchmark.

Then the question usually becomes: “What is a benchmark?”

It can be answered in the following way: It is a standard, a set of securities that represent a particular segment of the market and that are used for comparison and performance measurement purposes.

For example, the SMI is an index composed of the 20 top Swiss listed companies and is often used to assess the performance of the Swiss economy.

It can be easier to generate alpha in some asset classes than in others.

For instance, US equities are an asset class where it is very hard to find consistent portfolio managers generating alpha.

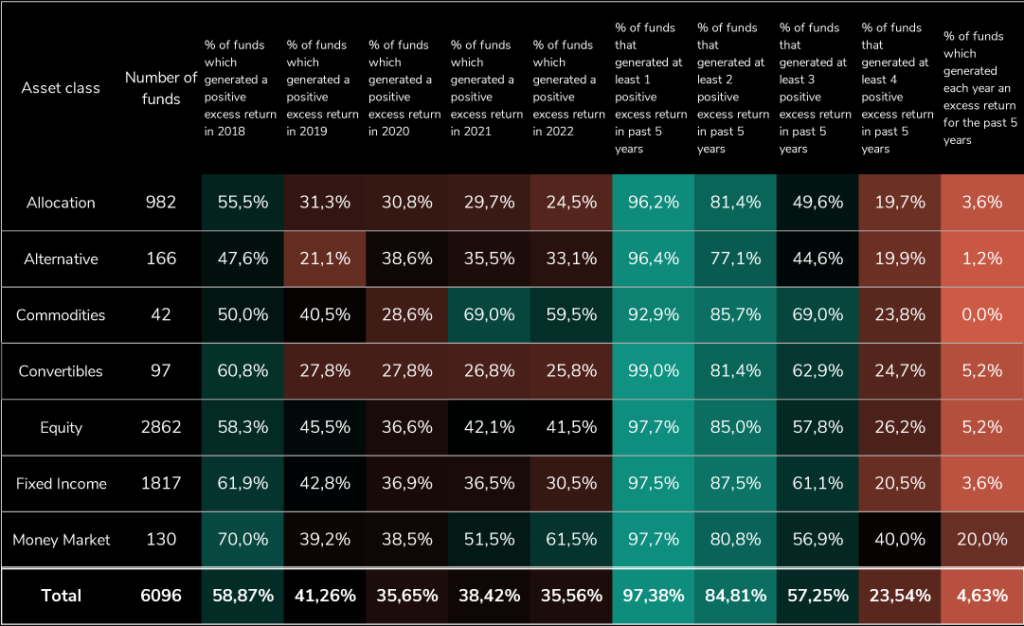

In order to illustrate that, we selected 8991 funds accessible by a Swiss investor and selected the 6096 with an existing return since 2018.

Then, we particularly focused on the returns of 2018, 2019, 2020, 2021, and 2022, and observed that if it was relatively common to generate alpha in 2018, 2019, or 2020 with for instance 59% of the funds that generated a positive return in 2018, 2020 was a much tougher year as only 35.65% of the funds generated a positive excess return, and 36% only in 2022.

While 2018, 2019, and 2021 were years where market volatility was in line with historical averages, 2020 and 2022 were more eventful. Extreme macroeconomic events such as the Covid crisis, the war in Ukraine, the rise of inflation, and the raise of interest rates make it more difficult for managers to adapt their strategies. As a consequence, more concentrated portfolios can suffer larger losses.

Worse, when it seems easy to generate at least one year of excess return, in the past 5 years with on average 97% of the funds which made it, there was only 5.2% of Equity and 3.6% of Fixed income funds which were able to generate a positive excess return each year since 2018.

It appears progressively difficult to generate alpha in a consistent way over the years.

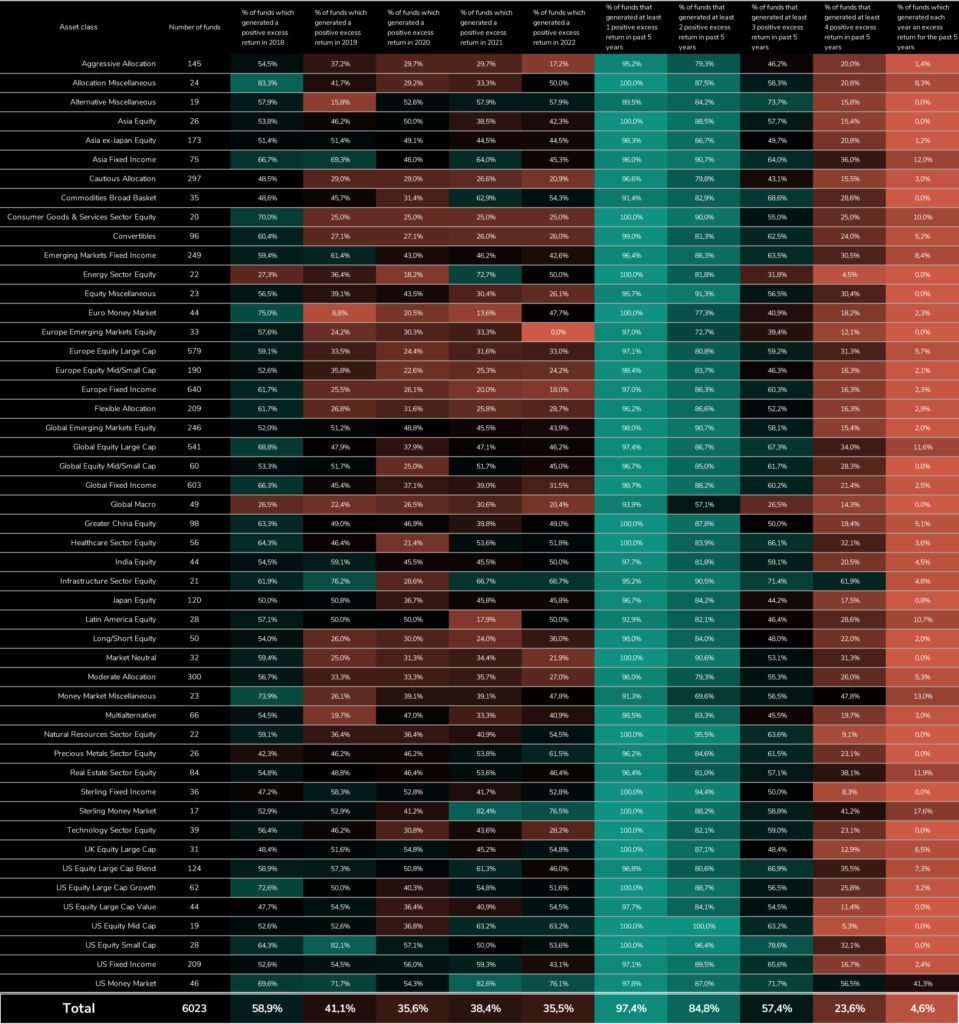

Furthermore, we dug to a more granular level and tried to understand if there were some specific sub-asset classes in which managers have more difficulties generating alpha. Our conclusions are the following:

Generating alpha seems more difficult in some asset classes than others, for example, no manager active in US equity large cap value outperformed the benchmark for the past 5 years in a row, whereas 12% of managers in Asia Fixed Income did so each year on the same period.

There may be several reasons for that: for instance, some asset classes are more niche than others. Some markets are less efficient and liquid, allowing managers to make a difference by carefully selecting securities, as opposed to buying the entire index universe. The more the quality and the amount of information increase, the harder it becomes for managers to outperform the market.

To conclude, if it seems feasible to generate alpha during the years when markets are reacting as anticipated, it is extremely hard to do it in a consistent way. Does it mean that you should absolutely avoid active investments? We don’t think so, as there is still added value in working with carefully selected managers. But you may want to adjust your expectations, depending on the asset class you seek exposure to.

Disclaimer:

The content of any publication on this website is for informational purposes only.